July 13, 2018

Policy Basics: Tax Equity

Tax adequacy measures whether the tax system provides enough revenue overall to build strong communities and economies where families can flourish. You can learn more about the adequacy of Virginia’s tax system in our paper A Tax System for Yesterday: Slow Revenue Growth amid Economic Change on how Virginia’s tax system is not keeping up with the economy.

Tax equity is a measure of the fairness of the tax system based on an individual’s ability to pay. There are two aspects of tax equity. The technical terms are horizontal equity and vertical equity.

Horizontal Equity

Horizontal equity–sometimes called “equal justice”–is concerned with equal treatment for those taxpayers in similar situations and with roughly equal ability to pay. For example, two families with the same incomes and family size should expect to pay the same amount in taxes. Inequity can occur here when a select group is able to take advantage of special deductions or tax exemptions that another group cannot.

Vertical Equity

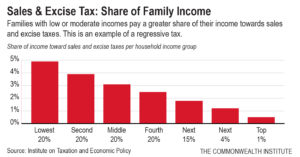

Vertical equity is concerned with tax rates paid by individuals and families with different abilities to pay. Ability to pay is often defined in terms of income. In other words, it considers how a tax might have different impacts on families with different incomes. For example, low- and middle-income families tend to spend a greater share of their incomes on necessities such as food, gas, and clothing. As a result they pay a higher share of their incomes on sales and excise taxes relative to high-income families. At the same time, the highest-income families pay a lower share of their incomes on those taxes. That’s because the tax is set and paid regardless of an individual’s ability to actually pay the tax.

Taxes that are set and paid with no consideration of an individual’s ability to pay and which result in situations where low-income families pay a higher share of their incomes toward taxes than high-income families, are known as “regressive” taxes. Common examples include sales tax, gas tax, cigarette and tobacco excise taxes, and taxes on groceries.

Alternatively, when high-income families pay a higher share of their income toward a tax than low-income people, those taxes are considered “progressive” taxes. A common example is the income tax — federal and state — which is structured so that the tax rate increases as incomes and ability to pay increase.

States rely on a mix of taxes with different implications for horizontal and vertical equity. In Virginia, the overall state and local tax system is highly reliant on state and local sales taxes, which are highly regressive, local property taxes, and a relatively flat — non-progressive — state income tax. The net result is that the lowest-income families pay a greater share of their income toward taxes than the highest-income families.