June 4, 2018

On Federal Tax Changes, Virginia Should Continue to Conform

Virginia lawmakers will face a decision at some point over how to respond to last year’s federal tax legislation and how federal changes will impact state income tax revenues. First, some context: As a share of the economy, state revenues are still not back to pre-recession levels which has led to large unmet needs in crucial areas like K-12 education, health care, and infrastructure. Deciding whether to conform to – or decouple from – federal legislation could mean the difference between hundreds of millions more in state revenues to invest in these key priorities or not. Legislators should not let this critical opportunity pass by. They should conform to the new tax law.

Since 2002, the General Assembly has routinely passed annual conformity bills to align the state tax code – with some exceptions – to federal tax changes made during the previous year. Like many other states, Virginia largely conforms for the sake of simplicity and ease of administration. To the extent possible, conformity allows residents and businesses to use one set of documents and calculations to prepare both their federal and state tax returns. In large part, filers and tax administrators are able to work off the same definitions, guidance, and other rules.

Most significantly in this case, by conforming to the recent federal tax changes, Virginia would see increased state revenues, primarily due to changes around federal deductions. Here’s why.

Many filers are expected to switch to the larger federal standard deduction – instead of itemizing deductions. Under state law, those filers must also claim the state standard deduction. Because this group will take smaller state deductions, state revenues will increase. At the same time, high-income households – those who are in the top 20 percent of income – who continue to itemize will see their deductions decline due to new federal limits around several deductions, such as those related to interest on mortgages and home equity loans, and a cap on the state and local tax (SALT) deduction. Conforming to the changes to itemized deductions would increase annual state revenues by over $100 million.

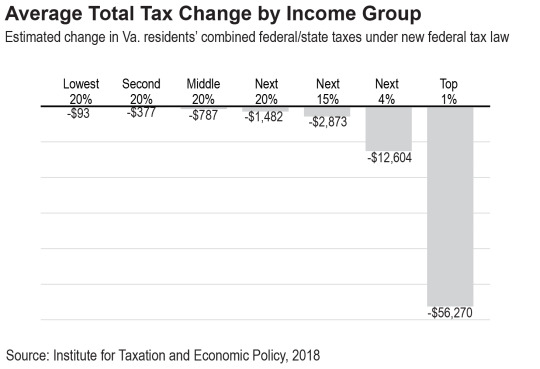

Although some filers would pay more in state taxes under conformity, many of the highest-income filers – the top one percent – will receive large state tax cuts. This is in addition to also receiving a large federal tax cut. Recent analysis of the effects in Virginia shows that the top 1 percent will receive larger federal tax cuts than the bottom 60 percent of households combined.

Much of the state tax cut for this group will be due to the elimination of a federal provision that limited the amount of many deductions that could be claimed by filers who exceeded certain income thresholds. Without those limits, filers in the top one percent will be able to claim additional deductions at the state level which could reduce state revenues by about $75 million annually.

Other states are already deciding on what action to take, and many are enacting broad state tax cuts in response rather than use additional revenue to strengthen public services or to provide targeted tax credits to low- and moderate-income working families.

Virginia should not go that route. While the federal tax cuts are tilted overwhelmingly to the wealthy, very high-income households, and large corporations, Virginia could use increased state revenues to make long-delayed investments in key areas like K-12 education that support the foundations for long-term prosperity, rather than pursue state tax cuts that would provide additional tax cuts for those same groups.

Despite important progress in recent budgets, state funding for K-12 public schools remains down 9.4 percent per student since the recession. This has had very real impacts in school classrooms like fewer teachers and staff. Since 2009, overall staffing in Virginia schools has declined by 1,242 positions while enrollment has grown by more than 50,000 students. This means larger class sizes and fewer supports for students. At the same time, the needs of students have also been changing. The number of economically disadvantaged students has increased by almost 90,000 students since 2009 and English learners in Virginia schools have increased by over 54,000.

State lawmakers could also choose to take a different approach to tax cuts. Rather than give more tax cuts to the highest earners and corporations, state lawmakers could instead improve the state’s existing working families tax credit – also called an Earned Income Tax Credit (EITC). By making this credit refundable, we would be providing tax relief to people who are working but have low incomes to put toward rent, groceries, and transportation, helping them make ends meet and bolstering their local communities. A targeted tax credit is one way to provide benefits to families who were largely left out from the federal tax law.

Virginia’s revenue system faces a number of structural problems that represent an ongoing challenge for keeping pace with the state’s needs. Although conforming to the new federal tax changes can’t fully address deeper issues, conformity would position the state to better meet crucial priorities.

Category:

Budget & Revenue