April 16, 2018

Point, Click, Dodge: How Online Sales Take a Bite Out of State Revenue

Tomorrow, the U.S. Supreme Court will hear arguments on a dispute between South Dakota and the online retailer Wayfair over whether Wayfair is responsible for collecting sales tax for purchases and sending it to the state. If the Supreme Court rules in favor of South Dakota, policymakers in Virginia and other states should take notice and act to make sure big multi-state online retailers are collecting and remitting sales tax for residents of their states.

Ever since the U.S. Supreme Court’s 1992 decision in Quill Corporation v. North Dakota, federal courts have interpreted the Commerce Clause as generally prohibiting states from requiring out-of-state retailers to collect sales tax. At the time, this ruling primarily applied to catalog sales. But with the rise of e-commerce, that precedent has had an increasingly significant impact on state and local revenues.

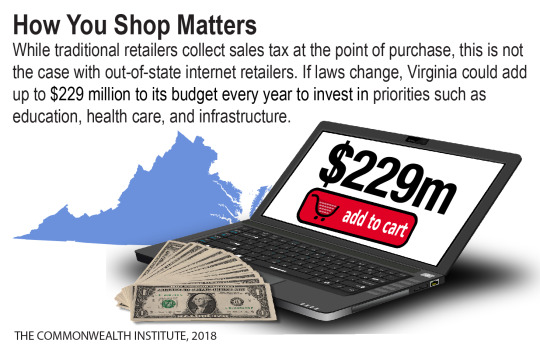

The net result has been less funding for priorities like education, health care, and infrastructure. Virginia misses out on an estimated $229 million annually due to e-commerce, according to an October 2017 report by

then state Secretary of Finance Ric Brown. Another estimate from the U.S. Government Accountability Office suggests that Virginia and its localities could stand to gain anywhere from $188 million to $298 million in additional revenue per year.

As a matter of principle, it’s unfair for some retailers to play by a different set of rules. The current system puts local brick-and-mortar stores at a distinct disadvantage. While traditional retailers are required to collect sales tax at the point of purchase, this isn’t the case with out-of-state internet retailers that have no physical presence in the state. Instead, customers are technically required to send the state any tax they owe related to their untaxed online and catalog purchases, but few do so. Placing the responsibility with the retailer, rather than the customer, would create a level playing field. And with technological advances, the burden on many retailers would be minimal.

But regardless of the outcome of the Supreme Court case, Virginia can take other steps forward on modernizing the tax code for the digital age. This past General Assembly session, lawmakers considered several such proposals, although none passed this year. HB1051 would have applied the existing communications sales and use tax, which already applies to cable TV and satellite TV and radio, to streaming audio and visual services such as Netflix. An early version of SB856, the Metro funding bill, would have extended Virginia sales tax to fares charged by transportation network companies like Uber and Lyft, which do not pay the same local taxes and fees as traditional taxis. Similar to the issue of giving an advantage to out-of-state internet retailers over local brick-and-mortar stores, it doesn’t make sense for our tax code to give certain businesses a leg up over competitors that offer a similar product or service.

As more and more of our economy shifts online, updating our tax code to keep pace with technological change means state and local revenues–and our public investments–can keep pace with the modern economy while maintaining a level playing field for businesses and consumers.

Category:

Budget & Revenue