August 16, 2018

Virginia’s Tax Choice: Another Break for the Rich or a Targeted Boost to Virginia’s Working Families

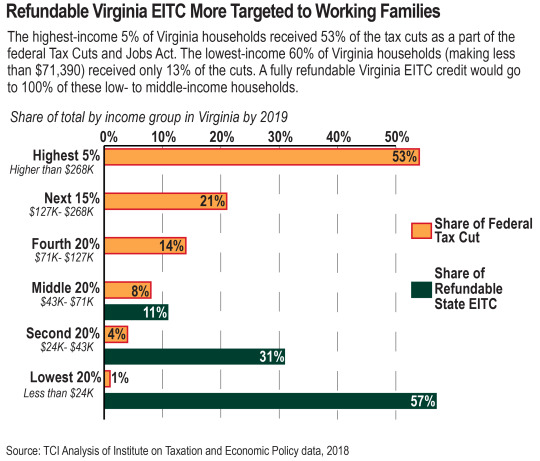

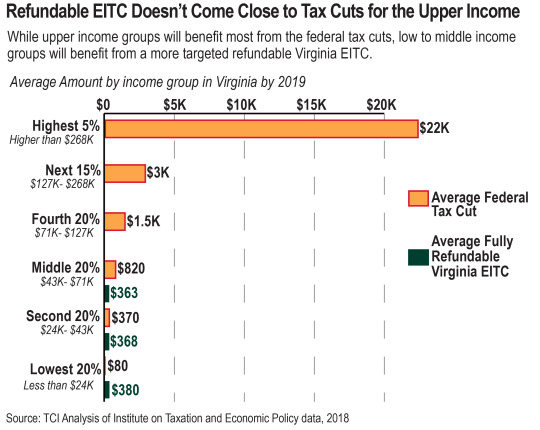

Virginia’s tax system is upside down. People earning low or moderate wages pay a higher share of their income in state and local taxes than the very wealthiest individuals, and most corporations pay no state corporate income taxes at all. Recent changes to federal law will provide large tax cuts to very high-income households, wealthy individuals, and profitable corporations, while many working families are left out. That’s why the governor’s recent proposal for a fully refundable state Earned Income Tax Credit (EITC) is a step in the right direction for tax fairness in Virginia.

Next year, Virginia will have a critical choice to make: what to do with the significant new revenue to the state from recent changes to federal tax law. Some estimates have indicated that these new revenues could be in the range of $500 million. The governor recently put forth a plan to invest nearly half of that revenue toward making the state’s EITC fully refundable – a credit that puts money back in the pockets of working Virginia families earning low-to-moderate wages. Currently the state credit is nonrefundable and families miss out on the full value of the credit they earned. Twenty-three states and D.C. have already made their state EITCs refundable, providing targeted tax relief to the hard working families in their states trying to make ends meet.

GOP leadership in Virginia were quick to counter the governor’s proposal with their own suggestion of using the new revenue to provide tax relief to “all Virginians” in the state, not just low- and moderate-income working families. But the highest-income families just got a major tax break from the federal tax bill. Most taxpayers of all income groups will receive a net tax cut in their total federal and state tax bill, with high-income people and corporations getting the biggest breaks – even though tax cuts for families with lower incomes have been shown to have a stronger relationship to employment growth.

Yet many working families will not receive a federal tax cut at all. A refundable state EITC represents a key step to help low- and middle-income families who received a small share of the overall federal tax cuts. Families with lower incomes spend more of their money locally. Targeting relief to low- and moderate-income working families through a refundable state EITC means that more will be spent in local communities – on education and on transportation to get to work – providing an economic boost to these families and the community as a whole.

Virginia has a critical choice to make: do we continue to invest in the wealthy, special interest groups, and corporations that benefited most from the federal tax cuts or do we make a pivot, and think about who will benefit most from tax relief and is most likely to reinvest it in our communities?

Category:

Budget & Revenue