September 13, 2017

We Need More than Wishful Thinking: A Closer Look at the Candidates’ Tax Plans

Helping create good jobs, making sure families can afford to buy groceries and other necessities, and building a better future for the next generation are important roles for state government. As Virginians turn their attention to the November state elections and discuss how to build that better future, it’s worth taking a deeper dive into how tax policy can help–or hurt–in shaping that future. And it’s important to do so in a clear-eyed manner, rather than relying on wishful thinking and unrealistic assumptions.

Issue platforms by the current candidates for Virginia Governor, including Republican candidate Ed Gillespie, Libertarian candidate Cliff Hyra, and Democratic candidate Ralph Northam, include proposals to modify or eliminate Virginia’s local business taxes, modify Virginia’s individual income tax, and eliminate the state portion of Virginia’s sales tax on groceries. All of these proposals would reduce local or state revenue collections. Given Virginia’s tight budget situation, when discussing the tax cuts it’s important to also discuss what public services would be eliminated or reduced or what sources of revenue will be raised to pay for them.

Local business tax cuts

Proposals:

All three candidates are proposing some change to the taxes that businesses pay to support city, county, and/or town public services, including the Business, Professional, and Occupational License tax, Machinery and Tools tax, and Merchant’s capital tax. The Northam campaign is proposing to exempt new startup businesses in rural or economically distressed localities from these taxes for two years. The Gillespie campaign takes a statewide approach, proposing to sunset the local business taxes and allow localities to re-enact either the same taxes or some alternative from a yet-to-be-defined menu of options. The Hyra campaign goes the farthest, proposing to simply eliminate the ability of local governments to levy these business taxes.

Impacts:

These taxes are frequent targets of “tax reform” proposals because, unlike the corporate income tax, they apply to gross receipts or inventory rather than corporate profits. However, they are a major source of revenue for local governments, raising over $900 million during fiscal year 2016, and local governments currently have limited ways to replace that money due to the state government not allowing them to levy local income taxes and other state-imposed restrictions. Reductions in local business tax revenue could impact the ability of Virginia’s cities, counties, and towns to provide basic services such as first responders as well as K-12 education, which on average accounts for over half of local government expenses.

Individual income tax cuts

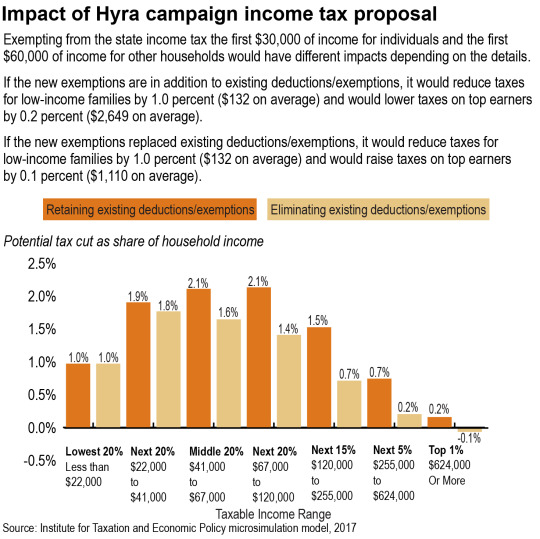

Two of the campaigns are proposing reductions in the state’s individual income tax. The Gillespie campaign is proposing to cut the current tax brackets by 10 percent, resulting in a 0.2 percentage point reduction to the lowest tax rate and a 0.6 reduction to the highest tax rate. The Hyra campaign is proposing to exempt from the state income tax the first $30,000 of income for individuals and the first $60,000 of income for other households, then retain the current 5.75 percent tax rate for income above those thresholds. (We have requested clarification from the Hyra campaign about whether the $30,000/$60,000 exemption is in addition to or replaces current exemptions and/or deductions, and have not yet received a response.)

New analysis by the Institute on Taxation and Economic Policy (ITEP) using their microsimulation model shows the impact of these income tax proposals on low-, moderate-, and high-income Virginia households.

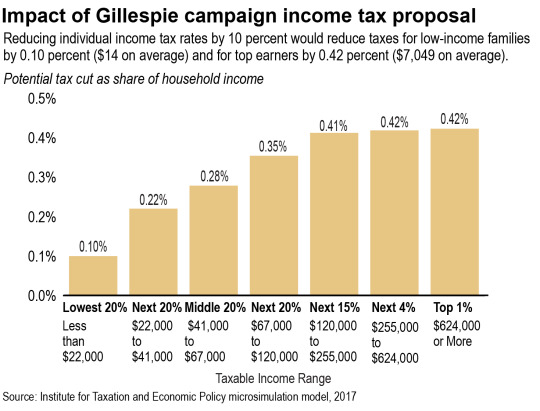

Gillespie’s plan and its impacts:

The Gillespie proposal would cost $1.4 billion when fully phased in and result in an average tax cut of $14 (0.1 percent of household income) for Virginia households with incomes less than $22,000, while providing a tax cut of over $7,000 (0.4 percent of household income) for the highest-income 1 percent of households who have annual incomes over $624,000. Middle-income households–those with incomes between $41,000 and $67,000 a year–would see an average tax cut of $147. (To get the $1,285 in estimated savings for a family of four stated by the Gillespie campaign, a household would need a gross income of over $229,000 or one would have to assume macroeconomic stimulus effects that are controversial among economists.)

Hyra’s plan and its impacts:

The Hyra proposal has different impacts depending on one’s assumptions about its details.

Using the assumption that they intend to eliminate all existing standard/itemized deductions, personal/ dependent exemptions, and personal income tax credits, and replace the existing rate and bracket structure with a new 5.75 percent rate on all adjusted gross income in excess of $30,000 (individual) or $60,000 (other households), the ITEP model shows the plan would cost Virginia $3.1 billion. This is in line with the campaign’s own estimate of the cost of their tax restructuring. These assumptions would result in an average tax cut of $132 (1.0 percent of household income) for Virginia households with incomes less than $22,000, while on average increasing taxes by $1,110 (0.1 percent of household income) for the highest-income 1 percent of households who have annual incomes over $624,000. Middle-income households–those with incomes between $41,000 and $67,000 a year–would see an average tax cut of $868.

Using the assumption that the Hyra plan retains existing deductions and exemptions, eliminates income tax credits, and replaces the existing rate and bracket structure with a new 5.75 percent rate on all taxable income (after deductions/exemptions) in excess of $30,000 (individual) or $60,000 (other households), the ITEP model shows the plan would cost $5.2 billion. This set of assumptions would result in an average tax cut of $132 (1.0 percent of household income) for Virginia households with incomes less than $22,000, while providing an average tax cut of $2,650 (0.2 percent of household income) for the highest-income 1 percent of households who have annual incomes over $624,000. Middle-income households–those with incomes between $41,000 and $67,000 a year–would see an average tax cut of $1,112.

The Northam campaign has not called for lowering state individual income taxes, instead proposing that a commission study Virginia’s tax structure and recommend reforms.

Grocery sales tax cut

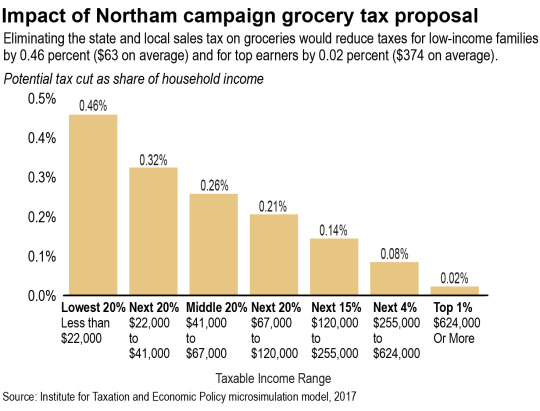

Northam’s plan and its impacts:

The Northam campaign is proposing “phasing out the regressive nature of the state grocery sales tax” as part of a broader tax reform package that would be created by a future tax reform commission. The state currently has a 1.5 percent sales tax on groceries, with localities getting another 1 percent for a total tax rate of 2.5 percent. Reducing or eliminating the sales tax on groceries for lower-income households but not higher-income households would be challenging to implement, since retailers would have to apply different tax rates to different customers, and as the Northam campaign notes most states fully exempt food from their sales tax.

ITEP analysis of the impact of eliminating the sales tax on groceries shows that it would cost the state $381 million when fully phased in. If the local sales tax on groceries were eliminated, it would cost local governments $254 million. If both the state and local portions of the sales tax on groceries were eliminated, low-income households would see an average tax cut of $63 (0.5 percent of household income) from such a change, while the highest-income 1 percent of households would see an average tax cut of $374 (less than 0.1 percent of household income). Middle-income households would see an average tax cut of $136.

Neither the Gillespie nor Hyra campaigns have proposed changes to the sales tax on groceries.

Tackling tax preferences and comprehensive tax reform

Gillespie’s and Hyra’s tax plans include language about eliminating tax preferences for special interests, while Northam has proposed tackling comprehensive tax reform. This is a welcome commitment and point of unity across the campaigns, and in theory could help pay for some of the proposed tax cuts. However, tackling tax preferences is easier said than done. Little progress has been made in the five years since JLARC–the legislature’s research staff–issued a critical report that identified many problems with the design and tracking of Virginia’s tax expenditures. It will take hard work on the part of the next governor and legislature to make these promises real.

Tax cuts impact public services

Any discussion of tax cuts should also include an honest conversation about what other taxes will be raised to offset them or what public services will be reduced. In recent decades lawmakers at state and federal levels have struggled to close enough loopholes to offset expensive cuts. The Gillespie campaign calls for revenue triggers meant to “ensure that Virginia can maintain its existing commitment to core services,” but revenue triggers ensure only that tax cuts are eventually enacted, making no such guarantee that Virginia’s revenues remain adequate to fund its growing public service needs. Virginia has been struggling with lower-than-expected revenue for years and it is unlikely that Virginia’s economy and state revenue will grow fast enough in the upcoming several years to finally restore public services to pre-recession levels, not to mention doing so while also paying for expensive tax cuts.

Given the underlying revenue challenges facing Virginia, the poor track record of attempts to close tax loopholes to offset tax cuts, and the difficulties associated with attempting significant tax reform, it is unlikely that any of the Gubernatorial candidates’ tax plans, if implemented, would be able to maintain funding at the levels assumed under current law. It’s most realistic, then, to take a look at what investments in Virginia’s future might be forgone and what services might be reduced to pay for the tax cuts each candidate has proposed.

Instead of a $1.4 billion tax cut, Virginia could choose all of the following and more:

- restore 4,000 teacher positions (to return Virginia’s teacher-student ratio to 2009 levels),

- pay for the state share of providing pre-kindergarten education to 49,000 children,

- provide 1,000 family and individual support waivers to help Virginians with serious disabilities stay in their homes,

- add 1,000 public mental health counselors and 1,000 substance abuse counselors to make real progress in fighting Virginia’s behavioral health crisis,

- provide Virginia’s share of metro capital funds,

- boost financial aid for Virginia students,

- and more.

As an alternative to a $380 million tax cut, Virginia could do the following:

- restore 1,000 teacher positions,

- pay for the state share of providing pre-kindergarten education to 13,000 children,

- provide 250 family and individual support waivers to help Virginians with serious disabilities stay in their homes,

- add 250 public mental health counselors and 250 substance abuse counselors to make real progress in fighting Virginia’s behavioral health crisis,

- provide Virginia’s share of metro capital funds,

- boost financial aid for Virginia students,

- and more.

A $3.1 or $5.2 billion tax cut would have an even more significant impact on Virginia’s public services than a smaller tax cut. Those amounts are larger than Virginia’s current combined general fund support for the following public services:

- Virginia’s colleges and universities, including community colleges,

- the state police,

- economic development and agriculture promotion,

- public health programs,

- and more.

Tax cuts sound good in a campaign platform, but their costs in foregone investment or cuts to public services must also be considered. Failure to do so amounts to basing public policy on nothing more than wishful thinking.

Category:

Budget & Revenue