January 22, 2026

Time to Reexamine Virginia’s Relationship with the Federal Tax Code

A fair and effective tax code is one of the most powerful tools to invest in communities, support democracy, and make sure everyone can thrive. Yet recent federal choices further concentrate wealth and power into the clutches of corporations and the wealthy elite who are already propped up by favorable tax policies. Governor Youngkin’s introduced budget chooses to double down on those harmful choices, tying Virginia’s future to tax breaks for large businesses, their rich shareholders, and wealthy individuals.

Continuing down this path would cost us about $465 million that could otherwise be invested in our public schools, affordable health care, and more at a time when there is very little revenues available for ongoing investment. In the coming weeks, state lawmakers will decide which federal tax changes to align the state’s tax code with. They should reject tax giveaways to wealthy corporations and individuals and instead use the state’s powerful ability to raise its own revenues, asking the wealthy to pay their fair share, and fund the programs that help communities thrive.

Why the Tax Conformity Debate is Happening Now

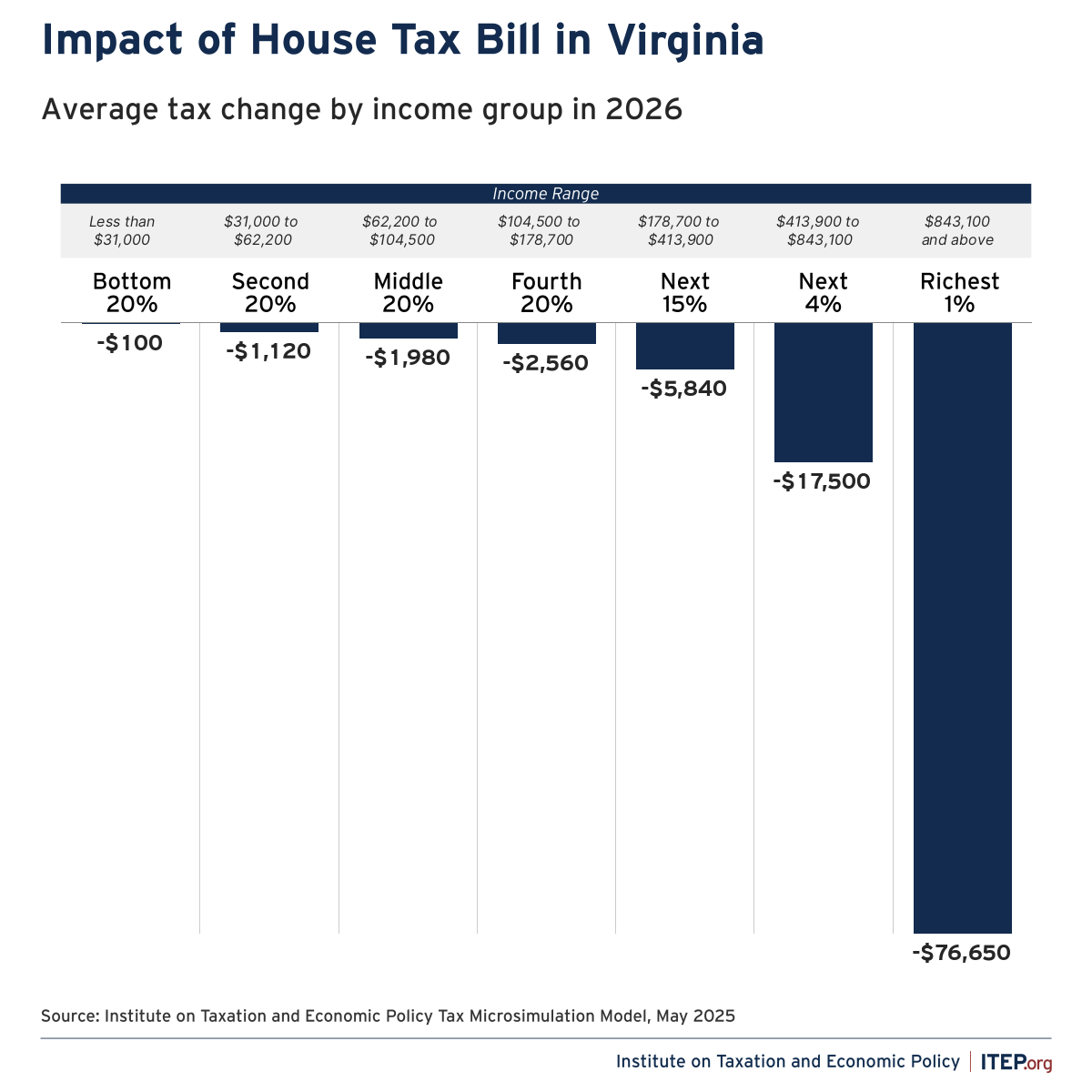

In summer 2025, federal lawmakers made many changes to the federal tax code through H.R. 1, which were designed to create windfalls for the wealthiest among us. The federal law will give an average tax cut of $78,530 to the richest 1% of Virginia households (making over $843,100). Not only will families who are paid the lowest incomes ($31,000 and below) get no tax cut, on average, the same federal package makes significant cuts to critical food and health care programs, and shifts some of these costs to the state. Changes to the federal tax code have implications for our state tax code, and doubling down on tax giveaways to the wealthy would mean the state forfeits hundreds of millions of revenues each year.

Lawmakers recently hit pause on Virginia’s typical choice to automatically adopt federal changes, with some exceptions. This means that lawmakers must now actively decide which tax provisions of H.R. 1 they want to adopt and which to reject.

Tax Conformity, Explained

When you file your Virginia state income taxes, you start with numbers from your federal tax return. The same is true for corporations, though the calculations and how you refer to them are slightly different. And this link — how the state uses federal rules and definitions as the baseline for state taxes — is called tax conformity. When federal lawmakers change how an individual’s or a corporation’s starting point is calculated, state lawmakers must decide whether to conform to those changes, as well as any other federal changes that flow through the state tax code, or break away from rules that don’t work for us.

What Governor Youngkin is Proposing

Governor Youngkin is proposing to adopt most of the tax changes in the federal bill (H.R.1) that flow through the state tax code. While the changes vary in design, they essentially have the same effect: tax giveaways to corporations and wealthy households at a high cost to all of us — about $465 million in the upcoming two-year budget cycle. Youngkin’s proposal would double down on substantial federal tax handouts for the wealthy few and further limit ongoing revenues that could be invested in critical community supports such as high-quality public education, accessible health care, and affordable housing. Lawmakers should instead protect state revenues and detach Virginia from harmful federal provisions.

Why These Choices Matter

Some of the most expensive conformity choices would increase or accelerate tax write-offs for businesses, allowing them to deduct costs immediately rather than over time and, in some instances, if following H.R.1 directly, retroactively.

The research and experimentation expenses proposal would give away tax benefits before the economic benefits of those investments are realized, creating windfalls for corporations while draining state revenues. While Governor Youngkin took a step in the right direction, and proposed to deconform from the retroactive provisions, Virginia lawmakers should maintain existing rules that spread the research and experimentation deduction over time, aligning tax benefits with actual economic returns.

In the case of the business interest deduction, Virginia conformed to changes in the 2017 tax law, but then allowed businesses to deduct some business interest that was not allowed at the federal level, up to 50% starting in 2024. There is no need to loosen the definitions like Congress did at the federal level, and Virginia should stick with its current rules.

In other cases, Virginia already has stronger protections in place. For example, like most other states, Virginia has not conformed to measures that would allow businesses to write off the full cost of certain property within its first service year (“bonus depreciation”) in the past. Breaking with this precedent would give tens of millions away to corporations, and lawmakers should reject this change. And while H.R. 1 introduces a new federal limit on itemized deductions for high-income filers, Virginia’s existing “Pease” limitation more effectively curbs the value of deductions for the wealthiest households. Forgoing this stronger state rule in favor of a weaker federal standard would create a tax break for high-income filers and reduce state revenues. Lawmakers should retain Virginia’s more effective limit.

The conformity debate also highlights federal tax preferences for capital gains that largely benefit wealthy investors, which should be re-examined, including Qualified Small Business Stock (QSBS) and Opportunity Zones. These programs allow people and businesses to avoid taxes on large portions of certain capital gains with little evidence that they deliver meaningful benefits to workers or communities — and because these start at the federal level, there is no requirement that the underlying investments even occur in Virginia. Continuing to conform to these provisions risks subsidizing out-of-state investment with foregone Virginia revenues. Lawmakers should not only deconform from the provisions laid out in H.R. 1, but fully end the special treatment of capital gains through these programs.

Virginia’s History with Conformity

While Virginia conforms to many parts of these calculations, we already make exceptions. For example, Virginia does not conform to several previous federal tax breaks, including special business write-offs and weakened limits on deductions that mainly benefit high-income households. In recent years, lawmakers have also adjusted how closely — and how automatically — Virginia follows federal tax changes.

Lawmakers adopted rolling conformity, meaning Virginia would automatically follow federal tax changes, but included guardrails to protect against dramatic revenue loss starting in January 2023.

And in 2025, lawmakers anticipated that new federal tax legislation would have potentially significant impacts on the state’s revenues, so they temporarily paused rolling conformity, with exceptions for extensions of existing tax policies, through 2026, essentially freezing the state’s tax rules based on what the federal code looked like on December 31, 2024.

What Conformity Does Not Include

Not all federal tax changes affect how we calculate individual income tax here in Virginia. Many federal choices, such as new exemptions for certain amounts of tipped or overtime income or changes to many tax credits, do not flow into Virginia law and, if added to Virginia law, would require state action separate from the conformity conversation. Virginia already makes its own choices in these areas, including maintaining its own standard deduction and personal exemptions. Even so, Governor Youngkin proposes to create new tax exemptions for tipped income, overtime income, and car loan interest based on the federal changes, at a cost of $271.8 million in state revenues.

Virginia lawmakers should not move forward with Governor Youngkin’s proposed partial deductions for tipped and overtime income. Exempting tips would create unequal treatment between workers despite similar incomes and leave many low-income families out, and exempting overtime could incentivize employers to pay lower wages and pressure workers to work more hours. Lawmakers should avoid narrow carveouts and instead take a broad, more fair, approach to reforming the state’s tax code.

Setting Out on Our Own

Relationships are complex, and the relationship between our state and federal tax codes is no exception. As negotiators debate what, if any, federal provisions we should adopt here in Virginia, they should avoid rehashing poor decisions made at the federal level. The choice is stark: a budget that reinforces unfair federal structures that give huge windfalls to the wealthy at the cost of investing in food and health care, or a budget that puts communities first and addresses their immediate needs.