November 14, 2016

Trouble in the Commonwealth

Virginia’s Revenue Problems Hurt Communities, and Can Be Addressed

Virginia’s schools, nursing homes, and local governments are facing another round of financial uncertainty as state policy makers debate how to fund these key priorities in the face of lower-than-expected revenue. And that’s just the short term. Looking over the longer term, Virginia’s revenue—the state’s ability to invest in schools, health care, and everything else that builds the foundation of strong communities—isn’t keeping up with the growing needs of a growing state.

State policymakers have a number of options before them, some of which will address the underlying problems and strengthen Virginia for the future, while others will just delay the problem for future years or continue damaging cuts to services Virginia families and businesses need to thrive.

Where Virginia Stands, And Why It Matters

The state’s revenue trouble is occurring despite a growing economy. There’s a lot that’s going well for Virginia’s economy these days. Unemployment is below 4 percent again. There are more jobs in Virginia than ever before. And many of Virginia’s new jobs are in the well-paying professional and business services industry. The tighter job market and growth in some well-paying industries is helping wages and incomes grow for typical Virginians. Median household income rose 2 percent in 2015, after adjusting for inflation. And 44,000 fewer Virginians than in 2014 have incomes that are below the poverty line, which is $24,257 for a family of four.

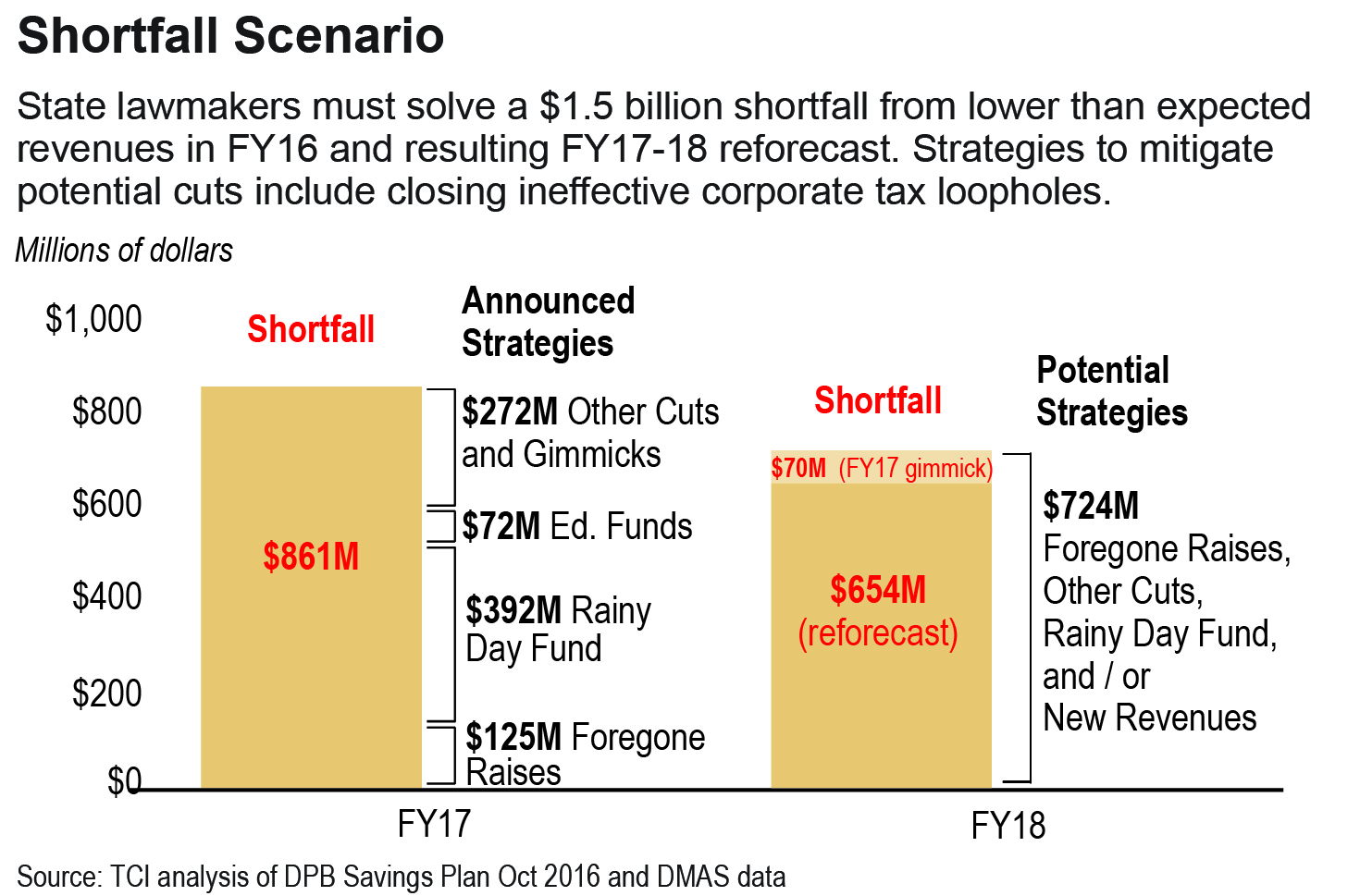

Despite these underlying signs of economic strength, state revenue collections are lagging. Virginia ended the 2015-2016 fiscal year with a shortfall due to state general fund revenue collections not meeting the forecasts that were built into the state budget. General fund revenue grew just 1.7 percent, compared to expected growth of 3.2 percent. That meant Virginia collected $279.3 million less during the 2016 budget year than expected. And because Virginia’s fiscal year 2016 revenue missed the mark, state policymakers have revised downward their projections of state revenue for the 2017 and 2018 fiscal years, creating a total revenue shortfall of $1.5 billion.

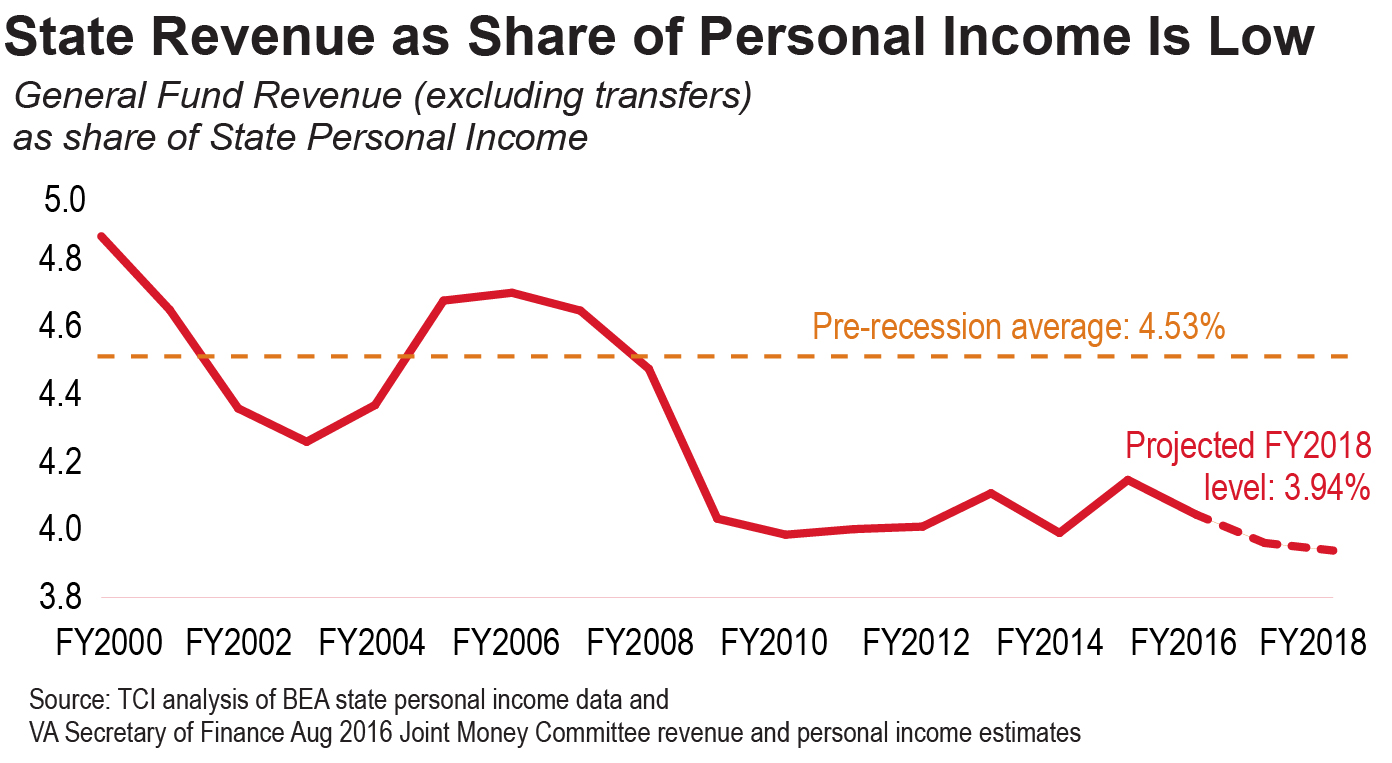

In the longer term, Virginia’s revenue is not keeping up with the state’s growing economy, creating long-term problems in funding critical services. State general fund revenue as a share of state personal income is hovering around 4 percent. That’s compared to a pre-recession average of 4.5 percent. If state revenues as a share of state personal income were back to the levels Virginia saw in the mid-2000s, it would provide over $2 billion a year to invest in the building blocks of a strong economy. Looking over the longer term, every year since the recession, Virginia’s tax revenue as a share of state personal income has been hovering at or below the lowest levels in decades. Virginia is now 43rd in the nation in state and local taxes as a share of personal income.

Both the short-term and long-term revenue challenges have real consequences for Virginians.

This fall, the governor announced a set of short-term actions in response to the fiscal year 2016 shortfall and lower 2017 revenue projections. Some of these will have real consequences in the short term. Using $72.1 million in higher-than-expected lottery revenues and educational fund balances to fill the budget hole leaves less money to enhance Virginia’s support for public education. Reducing support for state agencies delays the rollout of improved services. And cancelling pay raises for teachers and state employees makes it harder to attract and retain the most qualified employees. Some of the other cuts won’t cause short-term pain, but they will increase the likelihood of deeper cuts in the future, such as making a $392.3 million withdrawal from the state’s rainy day fund and suspending the rollback of Virginia’s “accelerated sales tax” budget gimmick.

In addition, some of the announced cuts, such as reducing the plan to carry over some general fund cash to help balance the 2018 budget, will deepen the cuts that have to be made for next year. Having already spent available fund balances and dipped into the state’s rainy day fund, the governor and General Assembly are likely to be faced with even tougher choices as they seek to fill a remaining gap of $724.3 million for the 2018 fiscal year budget that starts July 1, 2017.

One place they will likely look is to eliminate new initiatives that they first supported during the 2016 legislative session. Virginia’s colleges and universities have already been told by the governor to prepare plans to absorb a 7.5 percent cut from their state support. Policymakers may consider dipping into the state’s rainy day fund again, even though doing so makes it more likely that during the next recession Virginia won’t have a large enough balance to reasonably weather the storm.

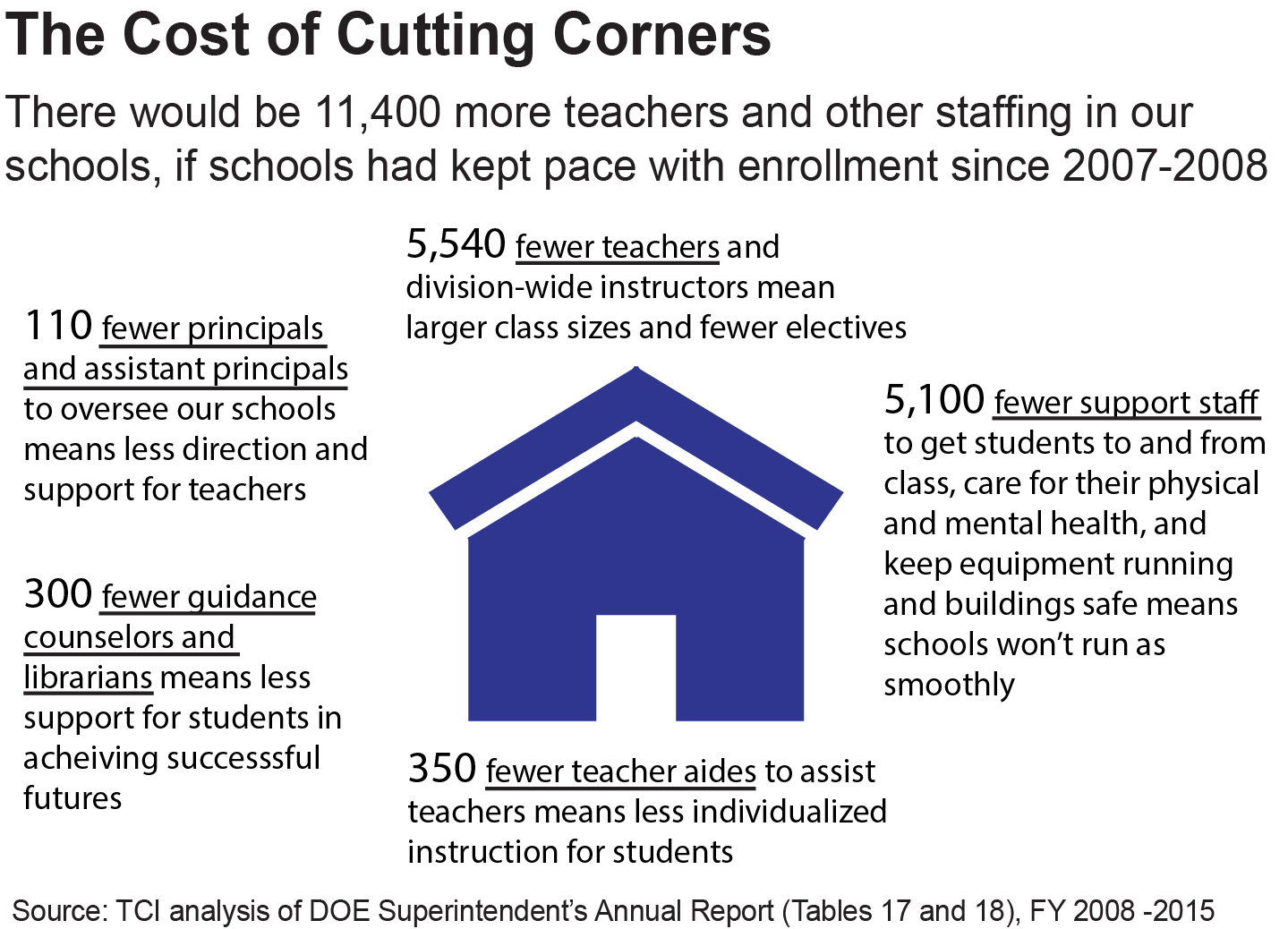

Virginia’s longer-term problem of lagging state revenue has even larger consequences for families and communities. Per-pupil state support for public education is down 11.5 percent since the 2008-2009 school year after adjusting for inflation. That’s a cut of $671 million. This has consequences even in relatively well-off suburban communities. In Prince William County, middle and high school class sizes have ballooned from 21 kids to 30 kids, and the school board’s final 2016-2017 budget cut in half the number of new behavior specialists and diagnosticians as a budget-balancing measure. In Chesterfield County, the school board has had to save money by not having nurses in all schools. The worst of the pain, however, is being felt in places where there are fewer local resources to fill in the gaps. With real consequences. In Brunswick, schools go days without a nurse and instructors are pulled from the classroom to treat health concerns. In Norfolk, there’s mold lining ceiling tiles, covering walls, and getting in the HVAC system. Recycling bins line the hallways when it rains to catch leaking water and teachers mop up what the bins miss with cardboard. Teachers and students are crammed three to a seat on field trips, because they don’t have enough bus drivers.

For students and families struggling to afford higher education, state funding cuts have also had a major impact. Per-student state support for higher education in Virginia is down 22.5 percent between fiscal years 2008 and 2016, when adjusted for inflation. This puts Virginia in the top third of states in the country with the most severe cuts in per-student state investment. As a result, Virginia’s public colleges and universities have increased tuition and mandatory fees sharply, placing a greater burden on students and their families. Between fiscal years 2008 and 2016, Virginia’s community colleges and 13 out of 15 of Virginia’s four-year public institutions increased tuition and mandatory fees for in-state students by 40 percent or more, even after adjusting for inflation.

Virginia’s communities and families are feeling the pain not because money is being spent on other priorities, but because the state is at or near historically low levels of public investment in the key building blocks of a strong economy. Even before any new reductions related to lower-than-expected revenue, general fund operating spending across Virginia’s two year budget was expected to be $7 billion below 2007 levels, after adjusting for the growing cost of providing the same level of services to a growing population. That’s more than $3 billion a year in reduced spending, a cut of more than 15 percent.

And Virginia’s mental and behavioral health system is so chronically underfunded that policymakers have not been able to implement much-needed improvements to increase access to community mental health services, despite bipartisan consensus that improvements must be made. Fewer than one in four young people in Virginia with major depression receive any mental health treatment, the third lowest rate in the country.

Identifying the Underlying Problem

If Virginia policymakers are going to effectively tackle the state’s short- and long-term problems, it’s important to first ask why revenue is lagging.

Short-term Fluctuations or Signs of Trouble?: Delving into the short-term story

In the short term, it’s not unusual for actual revenue to vary somewhat from projected revenue. Predicting the future is not easy. But it is somewhat surprising that this occurred even as key indicators of the health of the state’s economy grew faster than expected and faster than state revenue growth. According to estimates by Virginia’s Secretary of Finance, Virginia’s employment levels (up 2.3%), wages and salaries (up 4.2%), and personal income (up 4.3%) all grew faster than the 1.7 percent increase in revenue Virginia experienced during the 2015-2016 fiscal year. It’s possible this is the result of short-term fluctuations that will reverse—state revenue grew at a rapid pace during July and August, then fell in September—but it’s also worth considering other factors.

Personal income tax collections, which are Virginia’s most important source of revenue, were far slower than expected. Many Virginia policymakers have pointed to slow growth in jobs in middle-wage industries, and a concentration of new jobs in low-wage industries, as a possible cause of the state’s lower-than-expected income tax collections. Virginia’s lower-wage industries–those paying under $941 a week—did see faster total job growth than other industries during the 2015-2016 fiscal year. However, high-wage industries with average wages over $2,088 a week experienced reasonable job growth of 1.9 percent during the same time period, and Virginia’s strong 4.2 percent growth in wages and salaries is hard to square with an explanation that Virginia’s slow revenue growth is due to a shift to lower-wage jobs.

One possible explanation for slow income tax revenue growth is the rise of “independent contractors” and the “gig economy”—some of which is actually misclassification by employers of regular workers—rather than traditional jobs. Employer withholding and reporting is key to the high personal income tax compliance rate in the United States, and it’s possible that the drop in Virginia’s income tax collections may be a result of contractors (and misclassified employees) not reporting and paying their state income taxes, whether out of ignorance or deliberate negligence. Businesses who pay independent contractors more than $600 a year are supposed to report these payments to the IRS, but this often does not happen. Even before the latest uptick in “gig economy” jobs, JLARC estimated in 2010 that employee misclassification was impacting 214,000 Virginia workers and costing the state $28 million in lost income tax revenue.

Corporate income tax collections from big businesses plunged 10 percent during the budget year, partly driven by a plunge in corporate income taxes paid by the tobacco industry, even as the economy grew and corporate income tax revenue from small businesses rose 11 percent. Lower corporate profits may be partially responsible, since Virginia’s corporate income tax only applies to profits, but corporations may also have found new ways to avoid paying state income taxes.

In addition to lower-than-expected income tax collections, state sales tax revenue also grew slowly. This may reflect a shift in consumer preferences or a growing emphasis on savings, although it is too soon to tell if it’s just a temporary blip, and available national data does not show a higher personal savings rate during the 2016 fiscal year compared to the prior year.

Tax Avoidance and an Outdated Tax System: Delving into the long-term story

Longer-term, the reasons for Virginia’s lagging revenue as a share of the state’s economy are clearer. Virginia’s tax code has not been updated to keep up with changes in the state’s economy, and powerful interests are paying a lower share than in the past. Today, lower-income Virginians are paying a higher share of their income than the wealthy toward supporting the state’s schools, health care system, and roads.

Corporations are getting better at avoiding paying income taxes on their profits. One national study of 265 large corporations found that between 2008 and 2010, these companies paid state income taxes equal to only 3.0 percent of their U.S. profits, despite the average state corporate tax rate being 6.2 percent. Companies avoid paying state taxes on their profits through a variety of schemes, including lobbying for new tax loopholes and using subsidiary companies and gimmicks to shift profits into tax haven states.

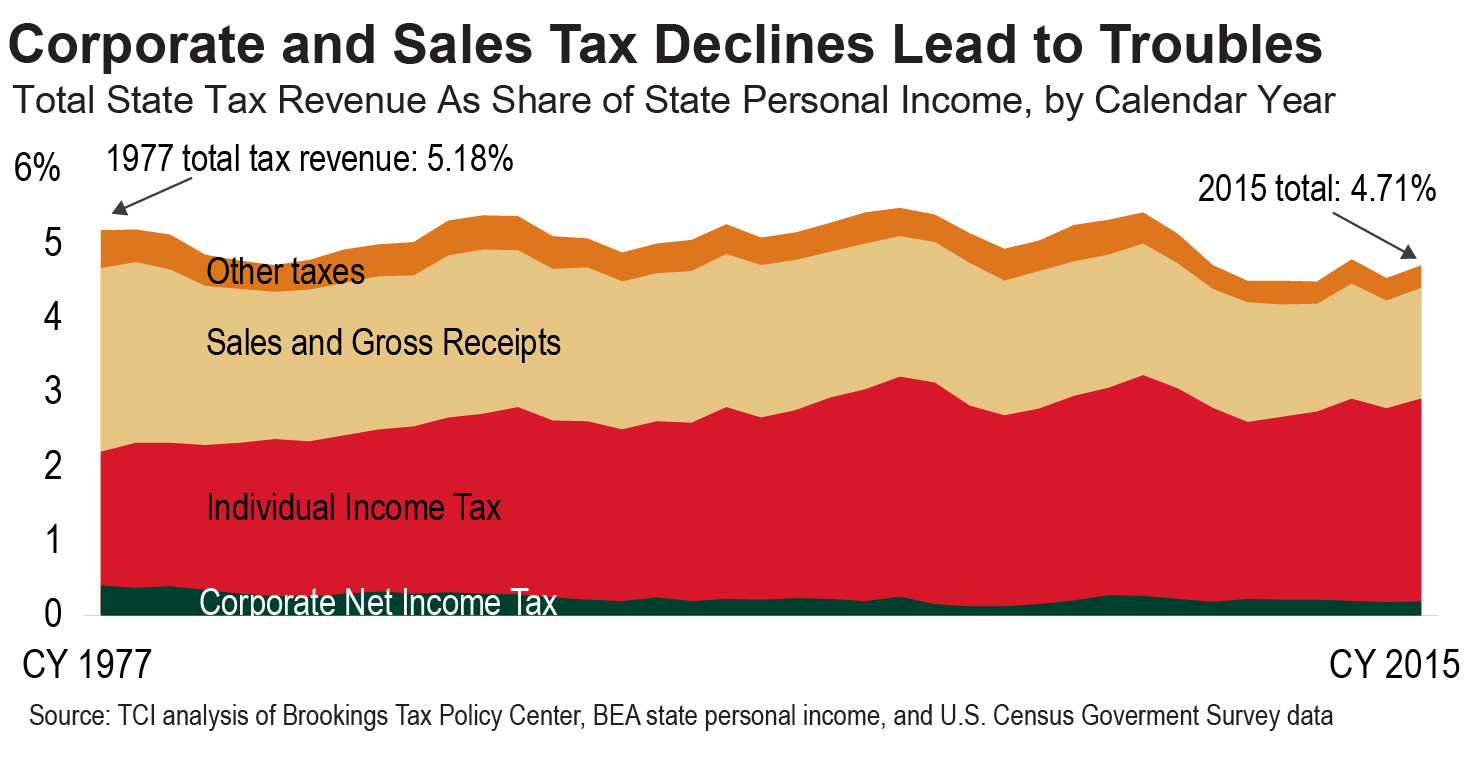

In Virginia, the impact of corporate tax avoidance can be seen in both the long-term decline in the share of state expenditures that are paid for through the corporate income tax and the decline in corporate income tax collections as a share of the state’s economy.

For decades, Virginia families have paid far more in Virginia income taxes than corporations, and in recent years corporations have been paying an even smaller share. While in 1980 the corporate income tax—which only applies to corporate profits—provided 15 percent of Virginia’s income tax revenue, by 2015 the corporate income tax provided just 6 percent of income tax revenue. Individuals and families, meanwhile, are paying more as a share of state personal income.

For the sales tax, as the country’s economy has shifted from the purchase of goods to the purchase of services Virginia’s sales tax hasn’t kept up. Virginia taxed just 18 of 168 services identified by the Federation of Tax Administrators in 2004, and has made little progress since that time. Meanwhile, sales tax revenue as a share of general fund revenue has plunged.

Solving the Problem

Facing a $1.5 billion total revenue shortfall, including a gap of $724 million that still needs to be filled, policymakers can and should use strategies that will strengthen Virginia’s long-term fiscal health and avoid more damaging cuts.

Virginia can take steps to reverse the long-term erosion of corporate income tax revenue by closing special-interest corporate tax loopholes and leveling the playing field for small Virginia businesses. These include Virginia’s failed experiment with the single-sales factor give-away, which costs the state about $59 million a year; eliminating the loophole where only part of the cost of hotel rooms is taxed if it’s booked through Priceline or other third party sites, which could provide over $2 million/year for the state’s general fund, plus more money for transportation and local governments; and working with neighboring states to end destructive race-to-the-bottom practices that help big multistate corporations at the expense of small homegrown businesses.

Cracking down on employee misclassification would benefit law-abiding businesses and workers as well as Virginia’s communities and families who deserve high-quality public services. The 2012 JLARC report on this topic made three recommendations of actions Virginia could take to prevent and catch employee misclassification, but these recommendations have not been fully implemented.

Policymakers should also take steps to make sure that wealthy households—which currently spend a lower share of their income on state and local taxes than middle-income Virginia households—pay their fair share. A good first step would be reforming Virginia’s neighborhood and educational improvement scholarship tax credits, which are so generous that wealthy individuals who are subject to the federal Alternative Minimum Tax or who donate appreciated securities can actually turn a profit from their “charitable” contributions. And in the long term, policymakers should update Virginia’s tax brackets and rates, which have not been updated since 1987, to better match today’s economy.

Finally, modernizing Virginia’s sales and use tax by extending it to cover more services could help make the sales tax more fair, particularly if policymakers were careful to target the expansion to cover services primarily used by higher-income households. Doing so would also bring Virginia more in line with other states, most of which tax a greater share of services than Virginia. However, any expansion of the sales tax to services should be coupled with measures to protect low-income households such as a refundable earned income tax credit, since sales taxes generally hit lower-income households harder than higher-income households.

Governor McAuliffe and the General Assembly can and should take a responsible approach to addressing Virginia’s revenue shortfall. In the short term, policymakers should close unfair tax loopholes rather than undermining needed support for Virginia’s already hurting schools and communities. In the long term, policymakers must address the underlying challenges facing Virginia, including making real reforms to the state’s outdated revenue system that is littered with breaks for often special interests and that is failing to keep up with Virginia’s growing and modernizing economy. Virginians deserve no less.