January 21, 2022

Youngkin Administration’s Proposals Would Sharply Reduce State Resources, Largely Exclude Working Families with the Lowest Incomes

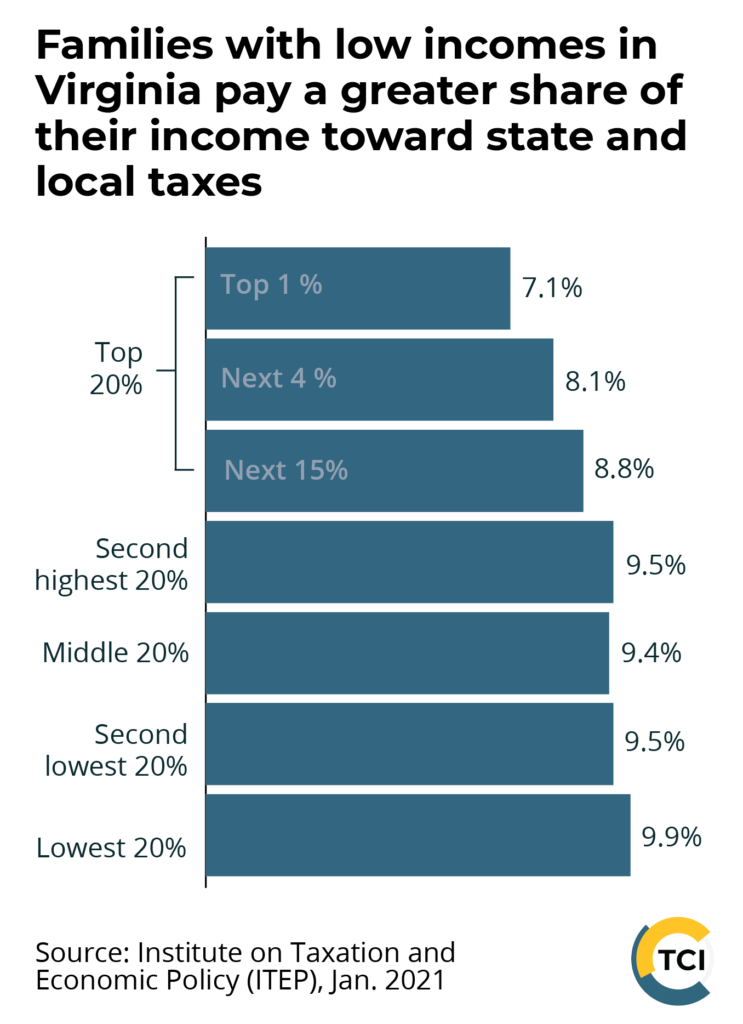

We all want a prosperous state with thriving communities. And our tax code can be a tool to advance racial and economic justice and raise the resources we need to achieve our shared goals. Yet Virginia’s tax code is upside-down, or regressive. Families and individuals with low and moderate incomes pay a larger share of their income in state and local taxes than those with the highest incomes. This is primarily driven by regressive taxes like sales, excise, and property taxes. The state tax code includes several policies to minimize state income taxes owed by many families with low incomes. But unlike other states that offer refundable tax credits for families, the impact of Virginia’s existing policies is limited because they do not offset state and local sales, excise, or property taxes. We must flip our upside-down tax code while also making sure the state has the resources to meet its funding commitments to education, health care, and other public services.

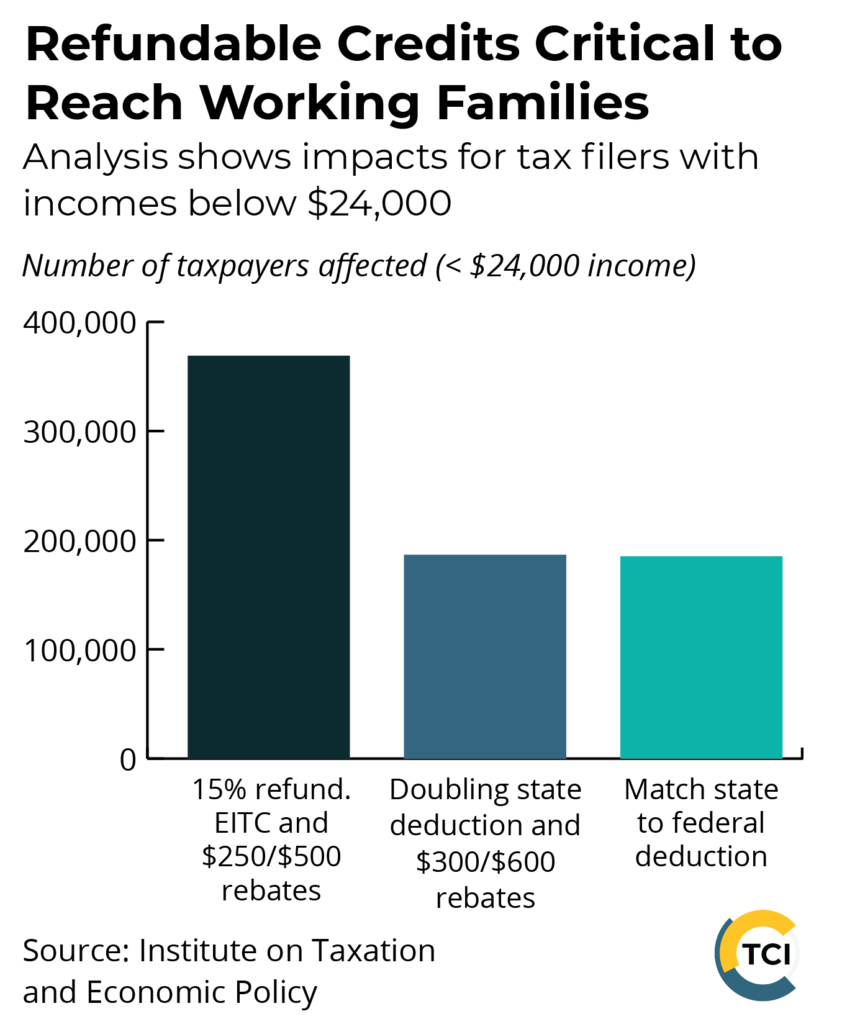

Both the Northam and Youngkin administrations have proposed tax rebates and substantial changes to Virginia’s income tax code, though the specifics of their plans vary considerably. While both proposals would lower taxes for many families in the state, the Youngkin administration’s plan would leave out nearly 80% of the over 800,000 taxpayers in Virginia who have incomes below $24,000. Gov. Youngkin’s proposed changes would also sharply reduce state General Fund revenues — the portion of the state budget over which lawmakers have the most discretion and which primarily goes toward funding K-12 and higher education and health and social services. Lawmakers should advance the policies that provide targeted support for families and preserve our shared resources for the long term.

The Northam administration proposed a targeted set of tax proposals that would address the impact of state and local sales, excise, or property taxes on people and families with low and moderate incomes, while having a smaller impact on the state budget than proposals to increase the state’s standard deduction. More specifically, former Gov. Northam’s proposal would eliminate the state’s portion of the sales tax that applies to groceries and personal hygiene products and make the state’s Earned Income Tax Credit (EITC) partially refundable for working families with low and moderate incomes, meaning those families would receive a larger tax refund.

The Virginia EITC is a state version of the federal EITC, a tax credit available to working families with incomes below certain levels, and the credit amount varies by filing status (single or married joint), family size, and income. About 600,000 working families in Virginia receive the federal EITC, and they are also able to receive a state EITC that matches up to 20% of their federal credit. Because Virginia’s state EITC is not refundable, most families who qualify for the credit do not receive the full amount of the state EITC, which would provide them a larger tax refund and help to offset sales, excise, and property taxes paid.

The state’s Commission to Examine Racial and Economic Inequity in Virginia Law recently recommended that the state enact a partially refundable EITC, noting that the policy “would help to increase incomes for working families in Virginia, particularly for Black and Latinx families who, and despite working, are more likely to be excluded from the current nonrefundable credit due to having low incomes.”

In contrast, the Youngkin administration has proposed doubling the state’s standard deduction. At least one bill before the General Assembly would enact this increase, while another bill would enact an even larger increase. These changes would largely not reach working families with low incomes.

Gov. Youngkin’s plan would leave behind so many families because the current state income tax code already includes several provisions that minimize state income taxes for individuals and families with low incomes:

- The state’s income tax filing thresholds are set at $11,950 for an individual or $23,900 for married joint filers. This is also known as the “no tax floor,” and tax filers with incomes below these levels do not owe state income tax and are not required to file a state income tax return.

- Qualifying tax filers can also claim either the state’s Low-income Taxpayer Credit (LITC) or a nonrefundable EITC.

The LITC is available to filers whose adjusted gross income is at or below the federal poverty level, which for 2021 was $26,500 for a household of four. The credit equals $300 per person, including the primary filer, spouse, and dependents.

As noted above, the state’s nonrefundable EITC reduces state income taxes owed for qualifying working families, but many are unable to receive the full amount of the credit.

Under one proposal, the state standard deduction would increase this year to $12,950 for an individual (up from $4,500) and $25,900 for a married couple (up from $9,000). These amounts are close to the existing “no tax floor” for state income tax, and many families already receive either the LITC or state EITC that reduces their state income taxes. As a result, by itself, increasing the state standard deduction would generally not help low-income families who may not owe state income taxes but, as noted above, pay a high share of their income toward other state and local taxes such as sales, excise, and property. Instead, increasing the standard deduction would primarily help middle-income tax filers and reduce resources for critical services.

We recently wrote about these issues and how to address the impact of the state’s sales tax on groceries and state fuels taxes with responsible, targeted solutions. While taxes that apply to groceries or motor fuels are regressive revenue sources, they currently fund important priorities and public services, including K-12 education, transportation, and other local services. Policymakers must work to pair any ongoing tax reductions with new, sustainable revenue streams, such as new tax rates that apply to millionaires or highly profitable corporations or modernizing the sales tax to apply to services.

To reduce taxes in a more targeted manner with less budgetary impact, state policymakers should consider the Northam administration’s proposal to make the state EITC partially refundable and eliminate the state portion of the sales tax on groceries. These policies could be paired with a much more modest increase to the state standard deduction. Lawmakers could also consider automatically adjusting the state standard deduction or personal exemption amounts to match inflation. A tax package that includes these elements would preserve a larger amount of budget resources, reach more tax filers with the lowest incomes who would otherwise not be reached by standard deduction changes alone, prevent inflation from eroding tax measures, and make the tax system more racially equitable.

Virginia’s state tax code is upside-down, but drastically increasing the standard deduction would create significant challenges for the state budget while excluding many taxpayers with lower incomes. The state must meet its commitments to public services like preK-12 education, health care, environmental protections, and other priorities. More targeted solutions would go further toward right-sizing the state tax code, while preserving state resources for the long term.

Categories:

Budget & Revenue, Economic Opportunity